Mr. Market has done it again with CoreCivic

Mr. Market has done it again with CoreCivic

a deep-dive, by Riccardo Formenti

26/09/2020

As the first piece of writing in my new newsletter, I wanted to dive deeper into a famous, dividend paying stock, that has helped made Warren Buffet a celebrity in the finance world: Coca Cola [KO].

KO’s fantastic moat, nice balance sheet, and a big fat generous dividend… Just messing with you guys.

We are actually going to look into a more exotic, unpopular, and controversial company, that better reflects my personality as an investor: CoreCivic [CXW].

You may be asking, why CXW? The answer is simple: the controversial nature of CoreCivic's business (among other things, the management of private prisons and correctional facilities) together with the recent conversion from REIT to C-Corp, has created an incredible spread between the intrinsic value of the company’s real estate and business fundamentals compared to its enterprise value. And there is also a catalyst, the 2020 US presidential election, which has the potential to greatly reduce this spread.

Let’s dive deeper…

Before continuing, allow me little bit of housekeeping:

Overview

CoreCivic is (as we’ll see later, “was”) a REIT that focuses on providing flexible real estate solutions to the US federal government, various government agencies and individual states (i.e. Alabama, California, etc.); in fact it is the largest private owner and manager of real estate for the US government.

The company has three reportable segments of operations: [1] Safety, [2] Community, and [3] Properties.

Source: CXW Q2 Supplemental financial disclosure

The Safety segment, which represents approximately 90% of last quarter revenue, includes 49 prison facilities, 42 of which are owned directly or through a long-term real estate leasing, under contract with federal agencies and individual states. These 49 facilities have a maximum capacity of 72,489 beds.

The Community segment, which represents approximately 5.5% of last quarter revenue, includes 27 rehabilitation facilities, either directly owned or through a long-term real estate leasing, with a maximum capacity of 5,233.

As of June 30, 2020, CXW had 9 unused (idle) facilities with a total capacity of 7,615 beds, which represents a short term growth opportunity in case of a contract assignment.

Source: CXW Q2 Supplemental financial disclosure

In addition to managing prisons and rehabilitation centers, CXW offers to government clients educational services with the aim of fighting against recidivism and preparing inmates to face the obstacles and difficulties that they may encounter once returning to society.

According to a report published by "RAND corporation" in 2016, inmates who, during their time in prison, participated in any educational program, are 43% less likely to return to prison. State authorities are aware of this important piece of data and are acting accordingly, as shown by the incredible demand CoreCivic is receiving for these types of services. These types of offering could be very important from a political point of view, as I will clarify later in the analysis.

And, last but not least, the Properties segment. Under this segment, CXW owns 57 real estate properties, totaling 3.3 million square feet, leased to government agencies through long-term contracts (including prisons owned by the company but managed directly by the U.S. government).

While these are the core businesses, CXW also operates two other subsidiary businesses that provide complementary services to the government: prison transportation services (TransCor America) and inmates monitoring via electronic bracelet and management of criminal cases / proceedings.

Although this is the starting point, management is shifting the company's focus in a very precise direction: properties. You can start to understand why by comparing this graph with the one seen a few paragraphs above:

Source: CXW Q2 Supplemental financial disclosure

One difference is glaring between the two graphs: the percentages represented respectively by the segments vary considerably, indicating very high margins for the Properties segment when compared to the other two. And this for a very simple reason: the expenses incurred by a landowner, who limits himself to renting a land with a building on it, are an order of magnitude lower than the expenses that he occurs when he has to worry about the land, the property, its maintenance, employees, inmates, etc.

If we look at the last few years we can see an incredible growth in the Properties segment Net Operating Income (24% CAGR) from 2017 to today, driven by M&A activities.

It is clear that management is expanding vigorously in this direction through M&A; however, higher margins are not the only reason: the other side of the coin is linked to the political risk (we’ll better understand later) which is intrinsic in operating private prisons but which does not exist in renting an office, for example, to the Michigan Department of Technology or any other government entity.

Competitive advantages, moat

As Warren Buffet said,

The most important thing [is] trying to find a business with a wide and long-lasting moat around it (...)

Let’s look at CoreCivic business:

Management, a business is just as good as its manager(s): Damon Hininger, CXW CEO, has served for the company for the last 27 years (!), starting as a correctional officer in one of the company’s facilities, working his way up to become the chief executive. You certainly could use some experience and know-how when operating private prisons and when dealing with big bureaucracy and big government.

Economies of scale: CoreCivic owns 59% of all private correctional facilities beds in the US and it is also the largest owner of buildings leased by the US Government (including Federal and State agencies).

The intrinsic nature of real estate: it’s incredibly expensive, both in terms of capital, hard-earned USD, as well as know-how, to build new projects from scratch, even more so when talking about complex and specialized assets such as CoreCivic’s facilities.

Risks

As with everything in the capital markets (and life), there are risks with CoreCivic:

Credit risk: in primis, interest rate exposure on some debt tranches on the balance sheet, around 40% of total liabilities.

But there’s also another side to the same coin: the difficulty, or even impossibility, in getting the credit in the first place. Starting after the 2016 presidential elections, some money center banks decided, after a “little push” by some democratic activist, to block all credit lines (and their renewal) to all companies in the private correctional sector (in CoreCivic case, starting in 2023).

Do not panic, there are alternatives: [1] with interest rates scrapping the zero level, and following Jay Powell declarations probably for a long time, there are rivers of private capital (not subject to the same pressure as big, publicly traded “evil” banks) ready to flood the debt markets in search of an higher than zero yield, as shown by CXW sale of $160,000,000 in bonds with a yield of 4.43% to finance a series of expansions projects in middle 2018, [2] the option of financing through complex capital structures (such as “DownReit”), as shown by the $83,000,000 in financing secured in January of 2020, [3] the option of receiving financing from banks outside the good ol’ US of A, as proved by $250 million in financing from a Japanese consortium led by Nomura in December 2019, and, last but not least [4] the possibility of a reversal in USA banks credit standards.

US government: the US government (state and federal, as well as various agencies) is the only customer for CoreCivic. While the probabilities of a US default are really low (FED going brrr), we have to account for that in our hunt for superior risk-adjusted returns.

Inflation: diving into the economics of CXW business, we can see how the majority of management contracts for correctional facilities include a fixed payment plus an extra for every inmate in the facility; but these contracts don’t account for escalators to fight possible inflation. The solution will be to renegotiate these deals after expiry.

Covid-19: while CoreCivic is much less affected by covid than other businesses, there still some risk in the pandemic: [1] being self insured and [2] a spike in cases inside prisons. The first risk arises from a company policy that consists in zero premium-derived payment to insurance brokers for car, health, and other work-related issues, therefore having to pay out of its own pockets any potential insurance claim. The risk lies in having to cover for employee health insurance. The second risk derives from an eventual spread of Covid-19 in CXW managed facilities. During last quarter CC, the CEO gave a little bit of color on this health-crisis: the virus did not have a material impact on the company’s operations. Never taking management word for granted, I fact checked these claims with data from the Bureau of Prison (BOP): there are currently only 1,995 inmates and 703 BOP staff who have tested positive for the virus nationwide.

Political risk: all another chapter dedicated.

Balance sheet

Let’s make a step backward and look at CoreCivic financial position; the balance sheet is in good shape, also taking into consideration the very nature of REITs (paying out 90%+ of net income as dividend; borrowing at a rate x, and investing in real estate trying to achieve a return of x + something) which tends to have more leverage than a normal companies:

All numbers in thousands of dollars ($ ‘000)

Source: CXW Q2 Supplemental financial disclosure and CXW Q2 10Q

As we can see, CoreCivic has $518 million in liquidity (including also the credit facility), and no debt maturing before October 2022, when $250 million of “5.0% Senior Unsecured Notes maturing October 2022” are set to expire, completely covered by present liquidity as well as cash generated from operations in the years to come.

And a closer look at debt maturities:

All numbers in thousands of dollars ($ ‘000)

Source: CXW Q2 Supplemental financial disclosure and CXW Q2 10Q

Source: CXW Q2 Supplemental financial disclosure

The big portion of outstanding debt will mature in 2023, precisely between April and May 2023. While we can’t predict what will happen 3 years from now, I think it is reasonable to expect that CXW will be able to meet its obligations in full considering [1] actual liquidity, [2] cash flow generated from operations, and [3] the possibility of debt refinancing.

It’s actually more representative to look at debt, excluding “Non recourse debt”:

Non-recourse debt is a type of loan secured by collateral, which is usually property. If the borrower defaults on this type of debt, the issuer can seize the collateral but cannot seek out the borrower for any further compensation, even if the collateral does not cover the full value of the defaulted amount.

Source: CXW Q2 Supplemental financial disclosure

Ultimately, CoreCivic has a good balance sheet, even better when compared to other REITs, with a leverage ratio (as calculated by [Debt, excluding “Non recourse debt”, - Cash and eq.] / EBITDA) of 3.7x and more than enough liquidity to cover debt obligations.

Cap. allocation - conversion from REIT to C-Corp

CoreCivic is a publicly-traded REIT, but not for long. On August 5, 2020, CXW management announced its intentions to convert the company from a REIT to a classic C-Corp.

We have to remember that CoreCivic was a C-corp prior to 2013; this corporate structure is known to management and employees.

To understand the motives behind this decision, and to understand if this is a good decision for CXW shareholders, let’s start from understanding what a company needs to do to comply to the REIT status; these are the main requirements:

A REIT must derive at least 75% of its gross income from real estate-related sources, such as rent, interest on mortgages or other MBSs, interest on other real estate related loans, sale of real estate assets,

75% of the total assets value of a REIT must be comprised of “real estate assets”,

Non-qualifying sources, like service fees or a non-real estate business, shouldn’t constitute more than 5% of a REIT’s income,

A REIT must pay at least 90% of its taxable income as a dividend to shareholders annually.

The main advantage of being a REIT is not having to pay federal income taxes on distributed net income.

But why did management elect themselves to convert to a TAXABLE C-Corp, basically why did they decide to pay more to Uncle Sam? Let’s walk through their reasoning:

CXW CEO Damon Hiniger during Q2 conference call, dated 08/06/2020

To be abundantly clear, we have not been satisfied with a trading multiple of our stock. For the past several years, our trading multiple whatever metric used to measure it has steadily declined, even as our earnings have grown like they did in 2019.

Continuing to pay a dividend yield [...] is simply not sustainable [at] recent trading multiple below 10 times, and certainly the current multiple low five times is not acceptable. It translates to a higher cost of capital inhibiting our ability to execute our business plan.

As a REIT, because we are required to distribute a substantial portion of our cash flows of dividends, we need to have continuous access to capital at reasonable prices to make investments at higher returns and our cost of capital.

[...] the cost of our capital has increased.

Provoking our REIT election will provide us more flexibility in how we allocate our substantial free cash flow. We believe the change in corporate structure will improve our overall credit profile [...] in our cost of capital.

This change in corporate structure will also give us with significantly more liquidity, which will enable us to reduce our reliance on the capital markets [...]

Because the company, as a REIT, is forced to pay a big portion of free cash flow in the form of dividends, they have to rely on capital markets, both equity and debt, to fund their operations and growth projects. This is standard REIT procedure. But here's where the problem arises: due to (overdone) pessimism in financial markets, CoreCivic's cost of capital has skyrocketed; looking at the equity side, you can buy the company’s shares at only ~5x FFO (!) with a 20% dividend yield, while different bonds maturities trade with yield of 7-8% at 70-80 cents on the dollar.

These rock bottom valuation, according to the company’s management (and to my research), do not reflect business fundamentals.

This underappreciation of the company’s fundamentals leads to higher cost of capital that leads in turn to problems in executing the company’s business model.

Fun fact, CXW pays in excess of $200,000,000 in dividend, every year, while trading at a billion dollar market cap.

The best way to solve this undervaluation problem is to divert excess cash flow from paying dividend to [1] delevering the balance sheet, [2] executing opportunistic buybacks, and [3] investing in attractive opportunities.

On last quarter conference call, CEO Damon Hiniger announced that CoreCivic intends to:

Pay down debt and deleveraging the balance sheet, which will in turn [1] reduce interest expenses and [2] improve the rating from credit agencies, further reducing cost of capital on the debt side. Management targets a 2.25-2.75x leverage ratio, as measured by ([Debt, excluding “Non recourse debt”, - Cash and eq.] / EBITDA). It currently stands at 3.7x.

Buyback shares at attractive valuation multiples while keeping leverage in check.

Invest in the property segment, well protected from political risk, like the recent Alabama project.

Invest in complementary non-real-estate businesses, such as inmate transportation or electronic monitoring, activities that were constrained under the REIT status.

To accelerate the new capital allocation strategy, CXW announced its intention to sell a portfolio of certain “non-core real estate assets” for ~$150 million, after related debt repayment. The sale is expected to be completed in late 2020 or early 2021.

While the C-corp conversion announcement should have been a positive catalyst for CoreCivic’s stock price, unlocking the opportunity for deleveraging and creation of shareholder value, the reality was different: a ~30% decline in five trading days. This sudden crash was probably caused by [1] uncertainty from market participants as well as [2] selling pressure from investors who need dividend income, as well as fund managers focused on income generating assets.

This (unjustified) drop only compounds the opportunity for savvy investors, looking for uncorrelated, market beating, returns.

But let’s dive into the numbers that justify all of these bold claims:

Valuation

In order to find the intrinsic value for CoreCivic, I used a couple of different models, based upon different metrics, assumptions, and methods.

The common denominator in every one of these models is “conservatism”. I deliberately lowballed my assumptions, added big margins of safety, and a lot of other valuation jargon, with the goal of accounting for the unexpected, for the risks I didn’t plan for.

“LBO inspired” model

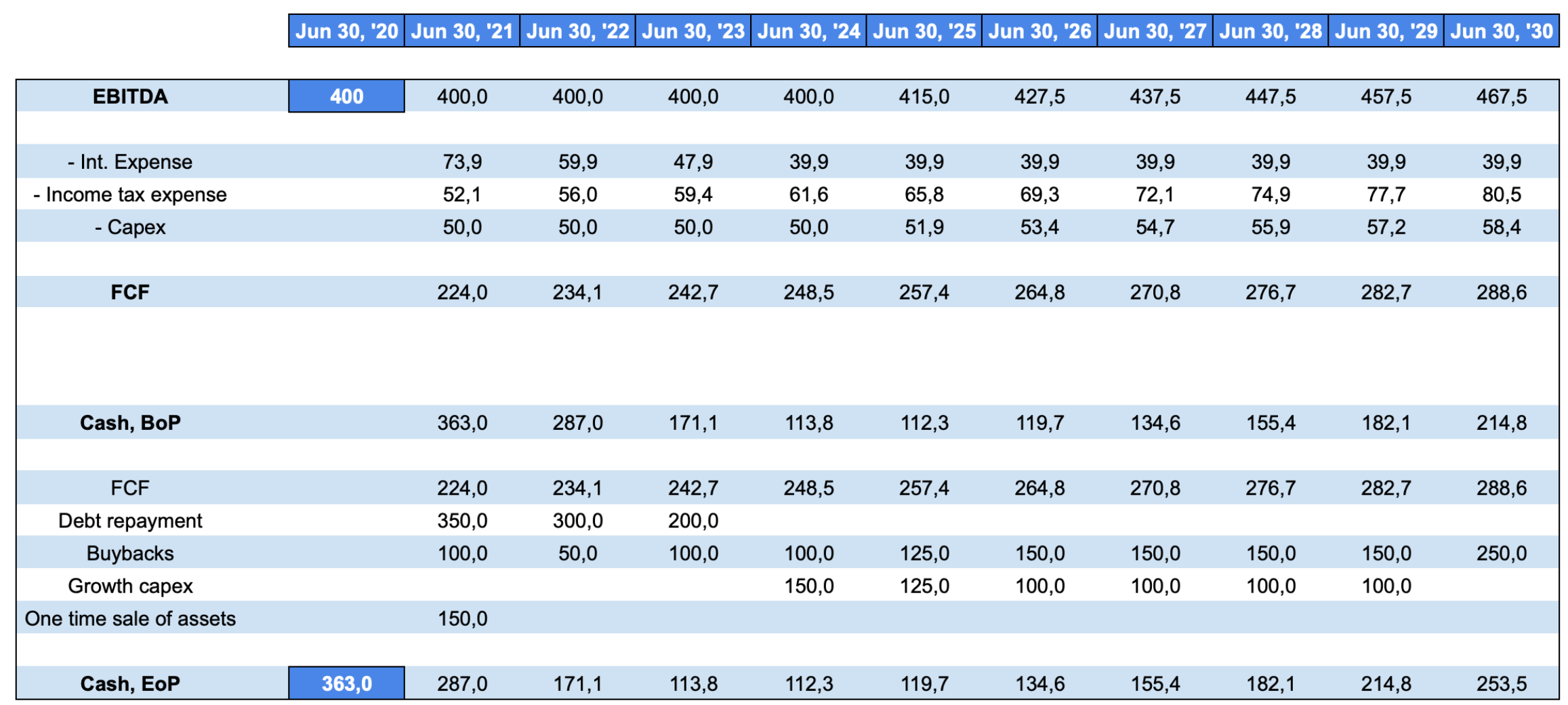

We start from EBITDA, and after subtracting “Int. expenses”, “Income tax”, and “Maintenance capex”, we arrive at Free cash flow to equity:

Formulas and explanation:

EBITDA = prior period EBITDA + growth capex * 0.10 (hypothetical ROI, based on CXW historical performances)

Int. expenses = Total debt outstanding, prior period * 0.04 (hypothetical weighted average interest rate, based on current 3.95%)

Income tax = (EBITDA - Int. expenses - D&A [yearly run rate of $140 mil., based on current $144 mil.]) * 0.28 (hypothetical corporate tax rate under a Biden adm.)

Maintenance capex = EBITDA * 0.125 (higher than current run rate of ~$35 mil.)

Free cash flow = EBITDA - Int. expenses - Income tax - Maintenance capex

We have generated cash, now we need to allocate it:

Formulas and explanation:

Cash, BoP = Cash, EoP, prior period

One time sale of assets = $150 mil. in 2021, as suggested by management during last quarter CC

Cash, EoP = Cash, BoP + FCF - Debt repayment - Buybacks - Growth capex + One time sale of assets

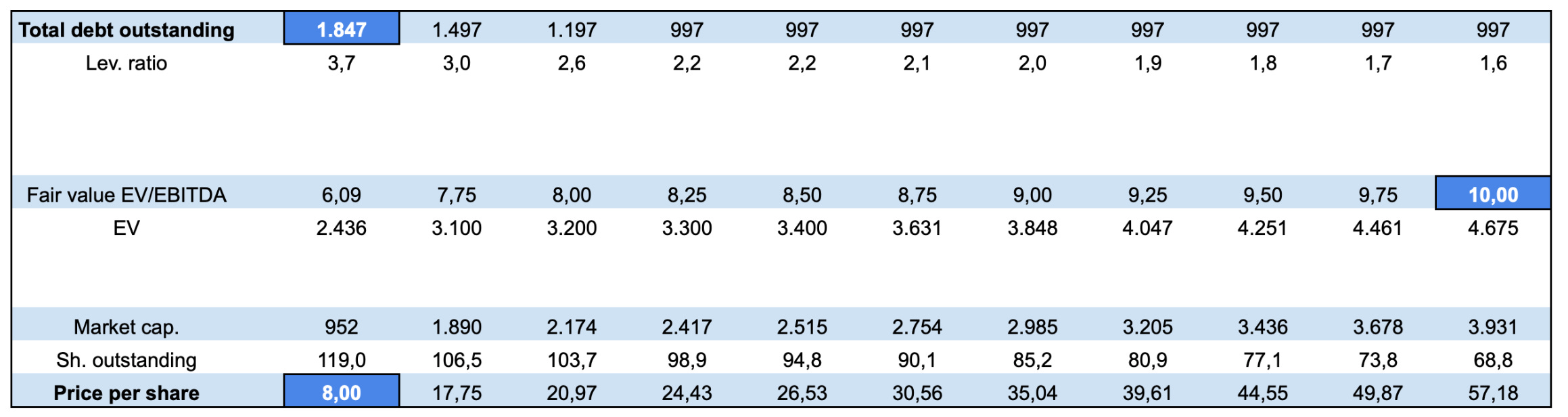

And to complete the full picture:

Formulas and explanation:

Total debt outstanding = Total debt outstanding, prior period - Debt repayment

Lev. ratio = (Total debt outstanding - Cash, EoP) / EBITDA

Fair value EV/EBITDA = starting at 7.75x, increasing by 0.25x each reporting period to arrive at 10x in 2030 (based on historical CXW average since 2013 of 10.3x)

EV = Fair value EV/EBITDA * EBITDA

Market cap. = EV - Total debt outstanding + Cash, EoP

Sh. outstanding = Sh. outstanding, prior period - (Buy backs / Price per share, prior period)

Price per share = Market cap. / Sh. outstanding

Here’s the actual math:

If you want to get access to the full model, do not hesitate and contact me

All numbers in millions of dollars ($ ‘000,000), apart from per share data

Starting assumptions:

EBITDA = $400, based on current run rate of ~$440,000,000

Cash, EoP = $363.0, Cash and Eq. from last 10Q

Total debt outstanding = $1,847, Total long term debt - Non recourse debt, from last 10Q

Fair value EV/EBITDA = 10x, based on historical CXW average since 2013 of 10.3x

Price per share = $8.0

Following management strategy from last quarter CC, I have modeled CoreCivic paying down debt in the first “phase” until achieving the target lev. ratio of 2.25x somewhere between 2022 and 2023, while allocating capital to shareholders through accretive buybacks. Starting in 2023, in the second “phase”, I modeled for a somewhere even split between investing into the business, represented by “Growth capex”, and returning capital to shareholders through buybacks.

If we then discount the terminal price per share of $57.18 to the present value by my required rate of return of 20% (yeah, pretty conservative), I arrive at a buy price of $9.24, a good ~10% above the current share price (keep in mind, to achieve a 20% CAGR for the next 10 years).

That’s what I call an opportunity.

Reverse-engineered DCF

Let’s start from a reverse-engineered DCF, a valuation method that allows us to estimate what kind of growth in FCF the market is pricing.

Here’s how it actually works: if the current market price implies the creation of more cash than what it is reasonable to expect from the company in the next 10 years, we can generally conclude that the stock is overvalued. If the opposite is true, we can generally conclude that the stock is undervalued.

This valuation method doesn’t have the big headache of every DCF: estimating future FCF growth rates. In fact, it’s a lot easier to verify the accuracy of what the market is pricing in than to create your own estimates based on a series of unknown factors and unpredictable events

Source: author’s assumptions and 2019 10K

A couple of comments:

The risk free rate is used is 2%.

I used an ultra-conservative exit multiplier of 5. In other words, this valuation is based on the assumption that CXW will trade at 5x FCF in 10 years, a multiple more common to bankrupted companies than good and stable businesses such as CoreCivic.

As of the last trading day, 09/25/2020, the market is pricing in a negative 23% CAGR in FCF for the next 10 years, a no-sense estimate considering past performances, the stability of the business as well as growth initiatives and future prospects.

Liquidation value

With every type of investment it is always important to account and model for the worst-case scenario, especially for companies like CXW, where the worst-case scenario is an outright ban on private prisons.

Looking deeper at CoreCivic, the worst case scenario is [1] Joe Biden, democratic candidate for president, wins the 2020 election in November with [2] enough margin on republicans in both the House and the Senate to pass the required legislation to ban the use of private prisons (at the federal as well as state level) along with [3] enough money in the budget to either build brand new facilities or, more probable and reasonable, to buy existing facilities from private owners (aka CoreCivic and GEO).

Our duty now is to get a grasp on the value of CXW’s real estate in the case of a ban and following buyout of private prisons: the problem here is that we can’t take the value of the “assets” on the balance sheet at face value because of a simple but important accounting tool: depreciation. The “property and equipment” value on the balance sheet is expressed at [cost - depreciation], while, in fact, real estate, particularly specialized real estate such as correctional facilities, appreciate over time.

We have to find an alternative: the company has around 65,000 owned beds in the safety segment, half of these in federal facilities, half in states facilities. Looking at recent projects, we can estimate the “cost per bed” (CPB) in the range of $200,000 to $400,000 at federal facilities and $100,000 to $200,000 at the state level. If, to remain conservative, we choose the low range state facilities estimate per bed for the entirety of beds (remember that half of these are federal, more expensive, beds), we arrive at an average CPB of $100,000. We also have a proxy for this number, a project from the state of Alabama: three new facilities totalling 10,000 beds for a price of $1,000,000, equal to a CPB of $100,000.

Here’s the math: 65,000 [beds] * $100,000 [CPB] = $6,500,000,000

But this is just the estimated value of the “safety” segment, which generates around 84% of total NOI. We also have to address the other two segments, “community” and “properties”; we decided to value these two segments at just 5x estimated 2019 FFO (FFO = NOI - g&a - int. expenses - taxes):

Note: I had to estimate FFO because CXW doesn’t break down FFO by segment but only NOI by segment; I calculated FFO by subtracting from NOI g&a, taxes, and interest expenses at the same ratio as they appear in the total. If, for example, “community” NOI is 10% of total NOI, we estimated that 10% of total g&a, interest, etc. belong to the “community” segment.

$17,119,000 [community NOI] * 5 + $33,187,000 [property NOI] * 5 = $251,530,000

Subtracting from the value of these assets that we just calculated all the liabilities on the balance sheet, and dividing the result by outstanding shares, we arrive at a liquidation value or, in other words, a (conservative) estimate of the value of CoreCivic assets to equity shareholders in the case of a ban on private prisons.

$6,500,000,000 [value of safety] + $251,530,000 [value of community and property] - $2,414,882,000 [total liabilities] = $4,336,648,000 / 119,164,000 (outstanding shares, diluted) = $36.4 (net asset value per share)

Just a note: I “forgot” to add the approximately $500,000,000 in cash;

Now, let’s apply on top of this conservatism another 30% margin of safety: we arrive at an estimated fair value per share of $25.

That’s what I call an opportunity, part. 2.

Politics, both a risk toward failure and a catalyst toward success

Disclaimer: this is politics. I commit to be totally unbiased, but it’s up to you to chose to continue reading. Caveat emptor.

Let's start with a fact: every company that earns money directly from the government, and that works with it, is intrinsically involved in politics, even more so when it comes to businesses with a controversial nature such as selling weapons or managing private prisons.

For CoreCivic the greatest risk that I believe the market is pricing in is that one related to politics. More specifically, some activist movements and some representatives of the Democratic Party that call for an outright ban on private prisons.

I believe that this fear is the exact reason why CXW stock trades at such a large discount to intrinsic value; our task is to understand how well-founded this fear is and if, consequently, we can take advantage of an exaggerated market reaction.

The events that the market now considers very likely are: [1] a Democrat will win the 2020 elections, probably in a landslide, [2] with the intention of banning the use of private prisons by states and federal agencies, [3] the right political conditions to execute that plan quickly will be set up.

Let’s break up this thesis:

The market is discounting a victory for Democratic candidate Joe Biden in the November 2020 election against Republican candidate, and current president, Donald Trump. But what are the real chances of this happening?

Right now Biden seems to be the most likely winner, according to almost every probabilistic model (The Economist statistic model, FiveThirtyEight, Financial Times). The average poll, by RealClearPolitics, paints the same picture. But looking at this study, assuming that polls are wrong by the same margin in the 2020 election as in 2016, during Trump v. Clinton, we arrive at a Trump landslide in November.

Predicting the results of political elections is something incredibly complex, and obviously it is not the goal of this report, if only for the simple fact that we do not need of Republican victory for the unfolding of our investment thesis. A Republican victory would simply be a catalyst that would accelerate the return on investment.

To better analyze a CXW investment, I excluded any favorable case and took Biden's victory in the 2020 elections as a given. The presidential candidate for the Democratic party has spoken out on occasion in favor of a ban on the use of private prisons, but often with conflicting ideas and certainly with less enthusiasm than other candidates such as Warren and Sanders.

In a political campaign that will no doubt be focused on Covid-19 and the economic effects of the lockdown, I do not see banning and destroying an efficient and taxpayer-friendly private sector as being one of the cornerstones of the political debate, as these graphs demonstrate.

Google Trends for the search term "private prisons":

As you can see, the interest of the population (measured by Google searches) in private prisons is at an all-time low, far from the peak reached in the autumn of 2016 during the previous presidential elections.

But, even if the use of private prisons were prohibited, the inmates in those prisons would not magically disappear, but would be transferred to other government-run facilities. And here the options become three: either [1] the federal government buys the structures from the owners (as we have already seen, scenario favorable to CoreCivic shareholders), or [2] the federal government decides to rent the structures from the owners (another favorable scenario), or [3] finally the government decides to build hundreds of structures from scratch. This last scenario is more suitable for a science fiction book than an investment article, considering the funds needed (billions) and the time needed (decades) to replace each private prison.

As we have seen, even in the worst-case scenario for CXW shareholders, that of a democratic victory followed by a federal ban on the use of private prisons, shareholders would end up benefiting from buying at the current prices.

If you’re interested in CXW revenue broken up by clients, here is the latest graph:

Source: CXW Q2 Supplemental financial disclosure

Buying strategy

As said by Dweight Eisenhower,

In preparing for battle I have always found that plans are useless, but planning is indispensable.

In the same way, it is of the utmost importance to strategize before entering any position in any asset class.

Looking at CoreCivic, there are 3 big, distinct paths: [1] straight buying into one of CXW debt tranches, [2] straight buying into CXW equity, and [3] building a position using derivatives.

The first two options are the most straightforward, with the debt more geared toward safety (in a bankruptcy scenario, debtors are the first in line to receive compensation) while equity is riskier, with greater returns.

But for my portfolio (this is not financial advice, by any means) I decided to take advantage of a known catalyst in the future, the 2020 race to the White House, and the intrinsic leverage in long call options to [1] maximize gains, to [2] allocate risk with accuracy, as well as [3] achieving outsized risk/reward. A quick glance at history show us this:

This picture represents CXW share price in the time frame June 2016 - July 2017. We can see a (almost) perfect correlation between share price and political results, with the yellow vertical line representing election night; after that, just a parabolic rise, that makes TSLA pales in comparison. And today, the situation is even better for possible CXW investors: [1] we have the opportunity to buy well below 2016 lows, and with [2] better revenues, income, liquidity position and overall balance sheet than compared to 4 years ago.

In particular, my position is built upon long call LEAPS, Long-Term Equity Anticipation Securities, a little forced upon acronym that indicates standard call/put options, with expiration at least 365 days out into the future.

I can briefly touch upon the fact that CXW can provide uncorrelated markets returns, not reliant on S&P 500, even less on NASDAQ, performances. We’ve been given by Mr. Market the rare opportunity to harvest an uncorrelated return stream.

Conclusions

CoreCivic is certainly a controversial company, but after an expected value calculation, probable returns far outweigh probable risks.

With a fair value around $25 per share, confirmed by two valuation models, and a buy price of $9.24 with a price target of $35 in the scenario of a republican win in 2020, I rate CXW as a BUY at ~$8 per share, as of 09/27/2020.

Thanks for reading.

Caveat emptor. Do not trust a 16 yrs. old on the internet. Do your own due diligence.

First and foremost: Great work, really appreciated your analysis and perspectives.

Allow me a few remarks, though:

- I think a lot of the pessimism towards CXW comes from the fact that over 10% of the beds are empty AND that US inmate numbers are flattening out, if not decreasing (see https://www.sentencingproject.org/wp-content/uploads/2020/08/Trends-in-US-Corrections.pdf). If this trend continues, it could lead to melting profits. And that's the crux of highly-specialized, expensive, moaty real estate - who wants to take an empty prison with high maintenance costs off your hands (except mad scientists)? Even Republicans could figure out that it is cheaper to send stoners trash picking instead of putting them into $100k+ uncomfortable beds.

- Not only ESG funds etc. are avoiding the stock, but soon REIT- and perhaps High-Div ETFs will have to follow suit. This could put some more pressure on the stock (which I assume you would sit out or even use to average down because this turmoil should be mostly over before your LEAPS expire).

- As much as I would love to jump into the stock (and most likely burn in hell), I remain cautious. It sounds compelling and the numbers are almost to good to be true. Alas, I have burned my fingers too often in similar situations. After all, the stock has lost more then 75% during the last 3.5 years and the performance before that has not been rosy either - so what are we missing here? Or is it a legitimate market inefficiency?

Outstanding good work!