New York! New York!

a deep-dive, by Riccardo Formenti

10/14/2020

2020 will be certainly reminded as an eventful year for the world, as well as for the metropolis of New York.

The city came to a halt in March 2020, when a viral agent started spreading among NYC and forced the local government to impose strict lockdown measures on the population, population that only now, after more than 6 months, is slowly being allowed to return to a “normal” life. It’s been more than 19 years since something so impactful happened to the city that never sleeps. You certainly remember what you were doing the morning of September 11, 2001 (I can’t, I wasn’t born yet, but I’ve read a lot on the events of that morning. Honor to all the first responders and average Joes who helped that day). But NY has recovered from 9/11, and will, in my opinion, recover from covid.

This pandemic-induced panic has sparkled an opportunity for savvy investors in publicly-traded NY multifamily real estate, better expressed through Clipper Realty, Inc. [CLPR].

Like Baron Rothschild famously said,

Buy when there’s blood on the streets.

Boring, but necessarily matters:

Do not fall for the “headlines” trap

Is it safe to invest in NY right now? NY, the epicentre of the pandemic? Are you crazy?

Recently, we’ve read all sort of scary and sensationalistic headlines about the future of New York and its real estate market. Titles such as “NY is dead forever”, by New York Post, and “A mad rush for the exits as New York City goes down the tubes”, by Fox Business, are all over the news. But remember, news companies are indeed companies, and as such they NEED to make a profit. They’re in the business of selling hype and fear, they’re in the business of selling exaggerated emotions.

But let’s check with reality and see how things are really going in the City (specifically in Manhattan and Brooklyn, where Clipper operates).

It is actually true that vacancy rates have increased and rents have decreased following the covid-induced lockdowns, but by how much? Is it really that bad?

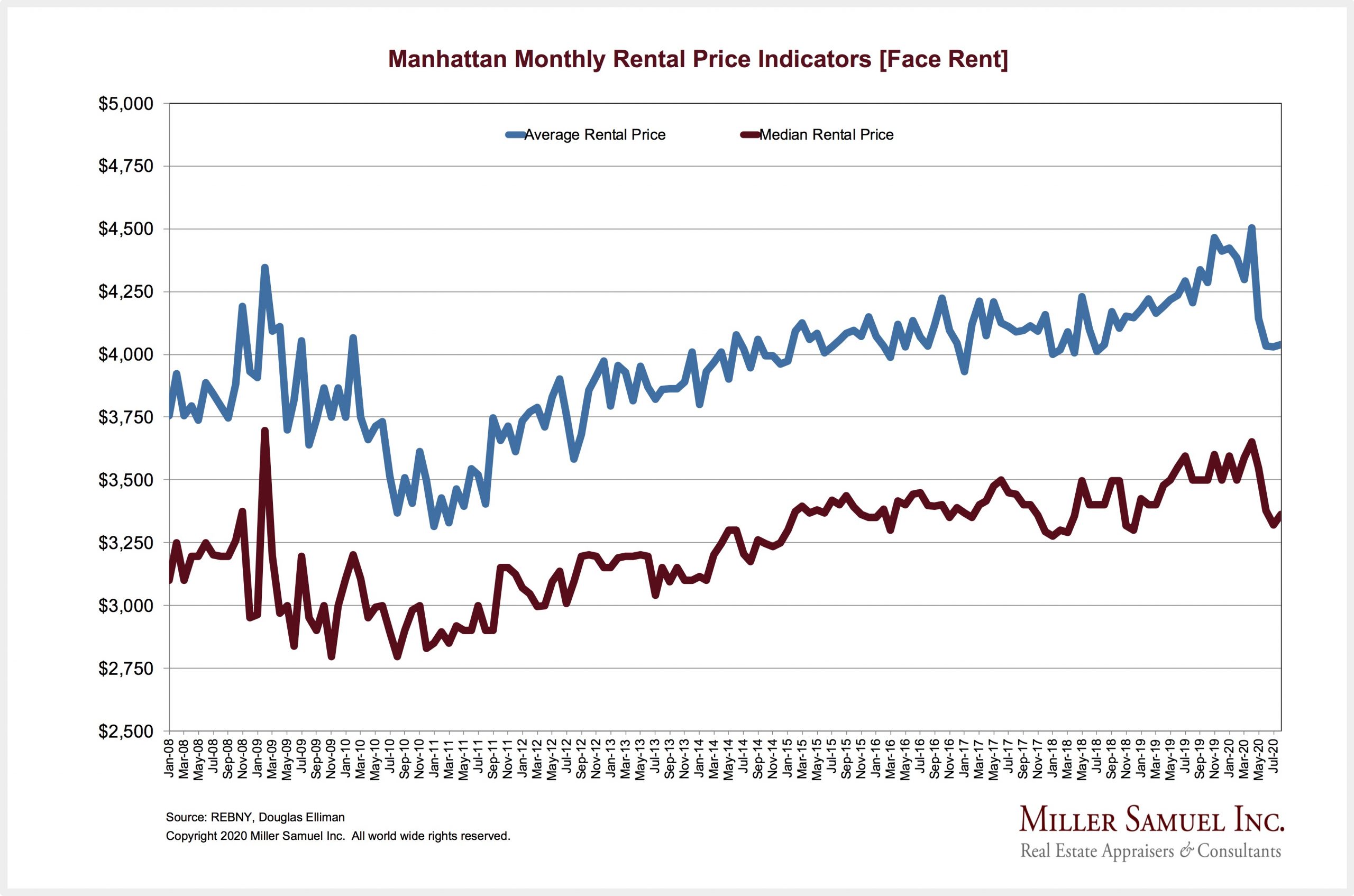

In Manhattan, as of September 2020, vacancy rates have increased to 5.75% from 1.95% a year ago while median rent has fallen by approximately ~8.0% YoY:

Source: Miller Samuel Sep. 2020 NY report and Manhattan rental price indicators

{kind=link}

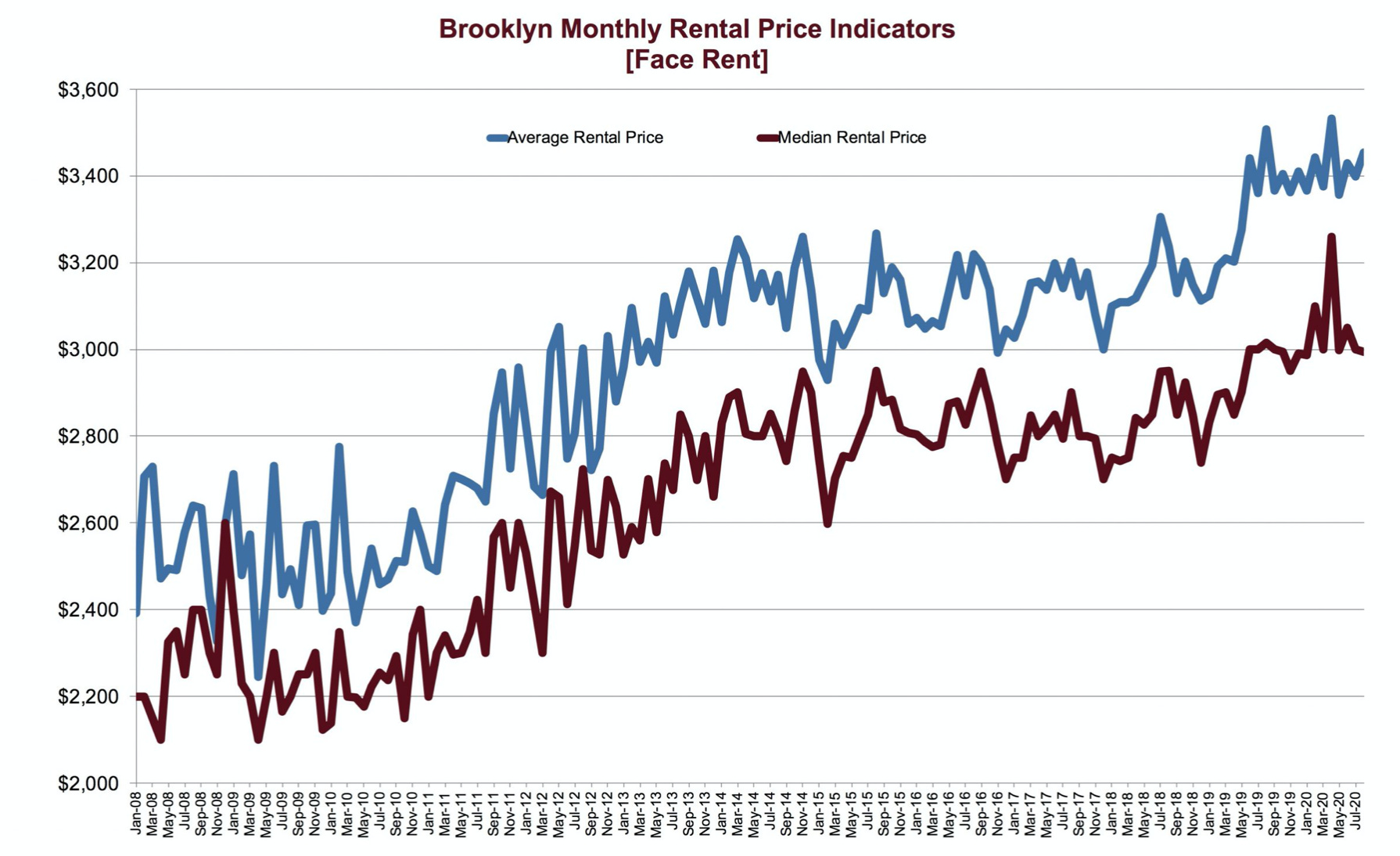

In Brooklyn, as of September 2020, vacancy rates are up approximately ~2.0% YoY while median rent has fallen by only ~1.7% YoY:

Source: Miller Samuel Sep. 2020 NY report and Brooklyn rental price indicators

{kind=link}

And how’s Clipper portfolio behaving?

Over 96% leased as of June 30, implying vacancy rates of ~4.0%, up from approximately ~2.0% a year ago. And because CLPR units were already rented at prices under market-level rent, this decline in median rent had a smaller impact. Revenue is actually up 8.0% compared to Q2 2019.

But the pandemic has also brought a positive for current multifamily owners:

Source: Yardi Matrix Summer 2020 Manhattan multifamily report

Source: Yardi Matrix Summer 2020 Brooklyn multifamily report

Supply growth is falling fast; this trend, coupled with increasing regulations, will mitigate the increasing vacancy rates in the City.

In a worst case scenario, CLPR has another advantage: all of its debt is non-recourse and non-cross-collateralized, meaning that every debt tranche is “anchored” to a specific property and, in case of a default, the lender can seize only the specific property and can’t touch any other assets. In other words, Clipper can literally walk away from any of its properties while continuing to earn rent from the other properties. This is flexibility, and I like it.

And besides, I don’t think NY is losing its appeal anytime soon.

A properties (and debt) analysis

Clipper Realty, a small-cap REIT that focuses on the NY City market, was incorporated in 2015 from the combination of a series of entities, among others a Berkshire (Buffet) subsidiary and a Reinessance Cap. (Jim Simons) subsidiary. Nice roaster of investors, don’t you think? CLPR owns a collection of 7 operating properties (plus 1 being developed as of Oct. 2020) totalling around 3.25MM leasable square feet, of which over 96% leased as of quarter end. Revenue is segmented in [1] residential, [2] office, and [3] retail:

Source: CLPR June 2020 investor presentation

Residential includes revenue from rent paid by tenants in the company’s multifamily properties.

Office includes revenue from rent paid by tenants in the company’s office properties, currently 100% leased to various departments of the City of New York.

Retail includes revenue from rent paid by tenants in the company’s retail properties, currently leased at a ~95% occupancy rate to quality tenants such as Starbucks and Apple bank.

And here is revenue, segmented by geography:

Source: CLPR June 2020 investor presentation

The company currently owns a portfolio of 8 properties, located in the NY metropolitan area, and financed through non-recourse, non-cross-collateralized debt.

Let’s dive deeper:

Flatbush Gardens

~35.3% of total revenue

All numbers as of 06/30/2020

Located in the East Flatbush neighbourhood of Brooklyn, Flatbush Gardens is a 59 building complex with a total of 2,496 units and 1.75MM square feet. The current rent per-square-foot (rent PSF) of ~$25 is lower than the market average of $30, and the property is 97.2% leased representing a 0% delta compared to pre-pandemic levels.

The property is financed through a $329,000,000, 12 yrs mortgage due in 2032 at a 3.125% rate and interest-only until 2027.

The company is in the late stage approval process with the City for the development of an additional ~500,000 residential sq. ft. that will add ~$12,500,000 to revenue (based on current $25 PSF) and ~$5,625,000 to NOI (based on current ~45% property level NOI margin).

Source: CLPR Q2 2020 supplemental financial disclosure and CLPR 2019 10K

Tribeca House - 50 Murray Street and 53 Park Place

~31.0% of total revenue

All numbers as of 06/30/2020

Located in Manhattan, Tribeca House includes two full service luxury buildings, at 50 Murray Street and 53 Park Place, with a total of 506 units, 428,000 residential square feet and 77,200 retail square feet. The current residential rent PSF is ~$70, compared to the market average of ~$80; the residential portion of the property is 91.3% leased representing a -8.3% delta compared to pre-pandemic levels. The current retail rent PSF is ~$44.

This is by far the most affected property by the crisis, but nevertheless the occupancy levels are well into the 90s.

The property is financed through a $360,000,000, 10 yrs mortgage due in 2028 at a 4.506% rate and interest-only for the entire term.

Source: CLPR Q2 2020 supplemental financial disclosure and CLPR 2019 10K

141 Livingston Street

~10.0% of total revenue

All numbers as of 06/30/2020

Located in Brooklyn, 141 Livingston Street is a 15-story office building with 206,084 commercial square feet currently 100% leased to the City of New York at a $40 PSF.

The property is financed through a $75,600,000, 10 yrs mortgage due in 2028 at a 3.875% rate.

Starting in 2021, under the lease contract with the City, rent will increase to $50 PSF, leading to a ~$2,100,000 increase in revenue and ~$1,480,000 increase in NOI (based on current ~70% property level NOI margin).

Source: CLPR Q2 2020 supplemental financial disclosure and CLPR 2019 10K

250 Livingston Street

~8.9% of total revenue

All numbers as of 06/30/2020

Located in Brooklyn, 250 Livingston Street is a 12-story commercial and residential building with 294,144 commercial square feet currently 100% leased to the City of New York at a $27 PSF and 26,819 residential square feet currently 94.4% leased at ~$46 PSF.

The property is financed through a $125,000,000, 10 yrs mortgage due in 2029 at a 3.63% rate and interest only for the entire term.

Starting in August 2020, under the lease contract with the City, rent has increased to $43 PSF from a base of 342,496 square feet, leading to a ~$5,000,000 increase in NOI (based on current ~70% property level NOI margin).

Source: CLPR Q2 2020 supplemental financial disclosure and CLPR 2019 10K

Aspen

~6.1% of total revenue

All numbers as of 06/30/2020

Located in Manhattan Upper East Side, Aspen is a 7-story building with a total of 232 units, 165,000 residential square feet and 21,200 retail square feet. The current residential rent PSF is ~$37; the residential portion of the property is 95.3% leased representing a -4.7% delta compared to pre-pandemic levels. The current retail rent PSF is ~$39.

The property is financed through a $70,000,000, 12 yrs mortgage due in 2028 at a 3.68% rate.

Source: CLPR Q2 2020 supplemental financial disclosure and CLPR 2019 10K

Clover House

~6.0% of total revenue

All numbers as of 06/30/2020

Located in Brooklyn Heights, Clover House is an 11-story building with a total of 158 units and 102,131 square feet. The current rent PSF is ~$72 and the property is 97.5% leased representing a -1.2% delta compared to pre-pandemic levels.

The property is financed through a $82,000,000, 10 yrs mortgage due in 2029 at a 3.53% rate and interest only for the entire term.

Source: CLPR Q2 2020 supplemental financial disclosure and CLPR 2019 10K

10 West 65th Street

~2.5% of total revenue

All numbers as of 06/30/2020

Located in Manhattan Upper West Side, walking distance from Central Park, 10 West 65th Street is a 6-story building with a total of 82 units and 76,000 square feet and 53,000 square feet of air rights. The current rent PSF is ~$41 and the property is 95.1% leased representing a +2.4% delta compared to pre-pandemic levels.

The property is financed through a $34,300,000, 10 yrs mortgage due in 2027 at a 3.375%.

Source: CLPR Q2 2020 supplemental financial disclosure and CLPR 2019 10K

1010 Pacific Street

~0.0% of total revenue

All numbers as of 06/30/2020

The company has recently filed plans to develop a 9-story, ~119,000 square feet, residential building in Brooklyn Prospect Heights, with a project deadline of approximately 2 years and a total cost of ~$85 mil. (including land already purchased for $31 mil.).

The property, being developed at a ~6.5% cap. rate, is expected to add approximately ~$5,500,000 in annual revenue and ~$2,000,000 in annual NOI, plus the opportunity to refinance the property at a lower cap. rate, unlocking further value.

Valuation

When talking about multifamily, the private market, not the public market, is the REAL market, as said beautifully by PrivateEyeCap. The majority of the assets are held by pension and endowment funds, other institutional investors, private equity fund (Blackstone with BREIT, KKR, etc.), and other wealthy investors, while the minority of assets are held by publicly traded REITs.

And after the March ‘20 crash, public and private returns have wandered in different directions: private real estate held steadily, public real estate fell hardly.

Source: BREIT report

This spread between public and private value cannot last forever. Either public markets will catch up or private investors will buyout publicly held assets.

Now the question is, how valuable is NY real estate in private markets?

The primary way to value real estate is the cap. rate: NOI / Assets value = Cap. Rate

To arrive at a fair assets value, we need an estimate of NOI as well as an estimate for a fair value cap. rate.

For the latter I decided to use a range of conservative estimate, between 4.25% and 5.25%, based on current US average, BREIT assumptions, and the recent refinancing deal brought forward by Clipper.

This specific deal warrants further attention as a valuation proxy: on May the 8th, at the high of the coronavirus pandemic, in NYC, the US pandemic hotspot, Clipper was able to refinance the Flatbush Gardens complex with a $329,000,000 12 yrs. non-recourse mortgage bearing a 3.125% interest rate. This deal allows the company to [1] save ~$3.0 mil. in annual interest expenses, [2] increase its cash position by $78 mil.

But even more insightful for us, in connection with this deal, an independent appraisal commissioned by the lender valued the property at $475,000,000. Annualizing Q2 2020 Flatbush Gardens NOI, we arrive at an incredible 4.1% cap. rate.

4.1% is the market value for CLPR properties, hence the conservative estimate range of 4.25% to 5.25% used in my valuation.

For NOI, we have to divide between: office, retail, and residential properties:

Because office properties are 100% leased to the City, with precise terms and rent escalation, I used the 2022 estimate at face value.

For retail properties, I decided to use 80% of fiscal 2019 NOI, assuming a permanent decline in NY retail rents and occupations levels.

For residential properties, I included a best case scenario, where all square footage expansion are built and rents reach market levels, a median case scenario, where rents stay flat at Q2 2020 levels, and a worst case scenario, where revenue falls by approximately ~32%.

Here’s the matrix:

If you want to get access to the full valuation model, do not hesitate and contact me

In green you can see positive share-price outcomes, in red negative ones.

If we then assume an equal distribution of probabilities between different share-price outcomes, I can compute an expected value for Clipper stock price: $11.30.

This $11.30 fair value is ~80% above the current market price of $6.30, as of 10/14/2020.

Now, I want to briefly introduce a new concept, the Kelly Formula (or Kelly Criterion), that will be the subject of my next article on “Almost Seventeen”. This formula, first used in professional gambling and then in hedge funds stuff (algos and quants, that sort of stuff), allows us to calculate the optimal portfolio allocation for every single bet (trade/investment).

The application of the Kelly Formula for CLPR results in a ~40% optimal position size.

To be more conservative, I usually use a 40% Kelly Formula, multiplying the standard result by .40. For CLPR, the optimal position size is ~16% of the overall stock portfolio.

Remember, I’m a contrarian investor who likes risk and a concentrated portfolio.

I will talk about the history, the application, and the computation of the Kelly Criterion in my next piece. Stay tuned.

Highly experienced, highly invested management team

With buying into CLPR comes also a highly experienced management team led by CEO David Bistricer together with board members such as:

Howard Lorber, Chairman of Douglas Elliman, the largest residential broker in NY;

Robert Ivanhoe, Co-Chair. of the REIT group at Greenberg Traurig;

Robert Verrone, former Co-Head at Wachovia’s Real Estate Group;

Harmon Spolan, former president at Jefferson Bank and current director at AEIG.

One of the things I like to see most in companies I want to invest into is alignment of interest between shareholders and management. This is certainly the case with CLPR, were directors own about ~55% of total outstanding shares and buying more as the stock was falling during the last few months, with only buy trades, in the $10-5.8 price range, totalling around ~$2.5 mil. worth of commons stock from CEO David Bistricer as well as directors Sam Levinson and Howard Lorber.

As if all of these wasn’t enough, with Q2 results the BoD announced an opportunistic $10 mil. buyback program, accounting for ~3.5% of total outstanding shares (assuming a pps of $6.5) and around ~7.7% of free float (!), adding further upside pressure to Clipper stock price.

Clipper’s experienced management team is definitely expressing its confidence in the company.

Source: CLPR SEC filings and Openinsider.com

Conclusions

Clipper owns a collection of quality assets in Manhattan and Brooklyn. While NY was the US hotspot for the coronavirus pandemic, I certainly believe that the City’s future will be bright. Data and history support this claim.

With an expected value of $11.30 calculated starting from private market prices, high (55%+) insider ownership, a recently announced stock buyback program, and flexible balance sheet built upon non-recourse debt, I rate CLPR as a BUY at current stock prices of $6.30, as of 10/14/2020.

Thanks for reading.

Caveat emptor. Do not trust a 16 yrs. old on the internet. Do your own due diligence.

I am curious to hear your take on the remote working paradigm (or hype?).

If remote working prevails on a broad basis, clearly this would dampen the outlook in the office space. But also residential (and by extension retail) could suffer because (a) no need to be close to the "workplace" and (b) the apartments in CLPR's portfolio are rather small - at least for standards I am used to. How are people supposed to pack a family and one or two office desks into a 600-700sf (~60-70m²) apartment (many apartments are even smaller)? If given a choice, I would prefer having a multi-screen setup instead of working from my kitchen table with a tiny notebook.

I am just wondering: Remote work mostly affects white collars, people who are usually in higher income brackets, i.e. exactly the type of clientele you want as tenants. If they get more bang for their buck elsewhere while retaining their nice salaries, why stay? For example, I am based in Vienna but living costs are much lower in my hometown, which is still large enough to be printed on maps and offers a high living standard including entertainment. If remote positions were ubiquitous, I would be very tempted to leave Vienna for good.

Or - grosso modo - office live will be back once this pandemic is over because

- cities are still attractive and people don't have enough space at home (circular with the above)

- lack of trust/oversight/power when not co-located

- failings to adopt efficient remote work culture/values

- hidden traps we don't (want to) see yet

- ...?

So, what do you think this means for city REITs?

Thanks for this well-written article! I'd be grateful if you could provide an excel version of the valuation table as well.