The miscategorization of R&D expenses and its impact on book value and earnings

The miscategorization of R&D expenses and its impact on book value and earnings

a short essay, by Riccardo Formenti

12/30/2020

Read in your browser

Choosing between capitalizing versus expensing different line items has a profound effect on reported financial statements for all sort of companies. As financial statements are the backbone of any analysis and valuation, it is important that they represent actual business reality instead of accountingesque reality.

Today we’ll explore the miscategorization of R&D expenses under US General Accepted Accounting Principles (GAAP), and its impact on the reported book value and earnings.

Under GAAP, R&D expenses are treated as "operating expenses", when, in fact, they represent "capital expenditures", and should be treated as such. This change ultimately affects all of the three financial statements.

While I've chosen to focus exclusively on pharmaceutical companies in this write-up, as R&D expenses are fundamental for their business model and represent a high percentage of revenue, the findings here presented can be extrapolated to all companies engaging in R&D spending.

FASB, 1974

In the US accounting framework there are two types of expenses (excluding financing expenses): [1] operating expenses and [2] capital expenses.

Operating expenses represent all expenses that a business incurs through normal operations to generate revenue and that provide benefits only for the current period. Cost of goods sold, SG&A, and marketing expenses are good examples, and appear entirely on the income statement.

Capital expenses, on the other hand, represents all investments whose expected benefit is longer than one reporting period. Capital expenses are recorded on the “cash from investing” section of the cash flow statement (capex), they create an asset on the balance sheet (PP&E) and are depreciated over their useful lives on the income statement.

But what actually is considered as R&D?

In October of 1974, the Financial Accounting Standards Board (FASB) issued the Statement of Financial Accounting Standards No. 2 (SFAS 2) requiring uniformity in the accounting of R&D:

Research is planned search or critical investigation aimed at discovery of new knowledge with the hope that such knowledge will be useful in developing a new product or service […] or a new process or technique […] or in bringing about a significant improvement to an existing product or process.

Development is the translation of research findings or other knowledge into a plan or design for a new product or process or for a significant improvement to an existing product or process whether intended for sale or use.

It includes the conceptual formulation, design, and testing of product alternatives, construction of prototypes, and operation of pilot plants. It does not include routine or periodic alterations to existing products, production lines, manufacturing processes, and other on-going operations even though those alterations may represent improvements and it does not include market research or market testing activities.

While R&D spending clearly provide benefits over multiple reporting periods, under SFAS 2 they are treated as operating expenses:

All research and development costs encompassed by this Statement [read above] shall be charged to expense when incurred [emphasis added]

The rationale behind this classification is that [1] there is high uncertainty about the future benefits of R&D spending, and [2] even if these benefits do materialise, it is difficult to quantify them.

Notwithstanding these arguments, expensing R&D results in erroneous measures of assets value (equity book value), earnings (net income), and profitability (return on equity) for firms who engage in considerable R&D spending. To better reflect the reality of a certain business, it is appropriate to capitalise R&D, creating a “research asset” on the balance sheet that will be amortized over its estimated useful life, resulting in adjusted measures for [1] book value, [2] net income, and [3] return on equity.

We’ll now look at the impact of capitalizing R&D, to account for the intangible created, on a number of pharmaceutical companies.

Case study: Pfizer, Inc.

I’ve chosen to focus on the pharmaceutical industry as R&D [1] represents a considerable amount of spending, [2] it’s central to the business model (no R&D, no drug to sell, no earnings), and [3] has shown to have the highest appropriation of any industry.

Appropriation of R&D benefits refers to the ability of a corporation to enforce its intellectual properties; its easier for Pfizer to enforce a patent on a clearly defined chemical formula for a new drug than for Snapchat to block competitors from copying a new successful feature (think of SNAP “stories”, now on Facebook, Instagram, WhatsApp, LinkedIn, Youtube…)

When capitalizing an expense we have to make a series of assumptions on the asset depreciation/amortization schedule.

For the pharma industry, I’ve chosen straight line amortization with a base line Estimated Amortizable Life (EAL) of 10 years (we’ll later explore the impact of changing EAL) and no salvage value.

10 years is an appropriate base line EAL as the usual process for FDA approval is cumbersome and lengthy; apart from this year extraordinary endeavour with the covid vaccine development, a standard FDA approval process lasts from 12 to 15 years.

Now let’s start with our case study: Pfizer, Inc.

Click here to download the model

The first step is to collect R&D data for a number of periods corresponding to the EAL, under the “R&D Expenses column”. We then have to calculate the “Unamortized portion” of each period spending:

equal to 1.00 for the current period, multiplied by current period R&D expenses;

equal to 1 - 1/EAL * period number, multiplied by period R&D expenses.

The sum of the “Unamortized portion” results in the value of the research asset, for Pfizer equal to $43.981 billion. That is, the reported book value of assets (and equity) is understated by approximately ~$44 billion.

The current period amortization charges is equal to the sum of each period amortization charges, calculated as each period R&D expenses multiplied by 1/EAL.

A look at the adjustments from a financial statements point of view:

As R&D spending is fully tax deductible under the Internal Revenue Code (IRC) there is no need to adjust taxes expenses.

By capitalizing R&D expenses we obtain:

Adjusted equity book value = equity book value + research asset

Adjusted net income = net income + R&D expenses - research asset amortization

Adjusted return on equity = Adj. net income / Adj. book value

To measure the impact of capitalizing R&D, I’ve introduced three metrics:

Book value “Multiple” = Adjusted book value / Equity book value

Net income “Multiple” = Adjusted net income / Net income

∆ (adj. - rep.) = Adjusted return on equity - Return on equity

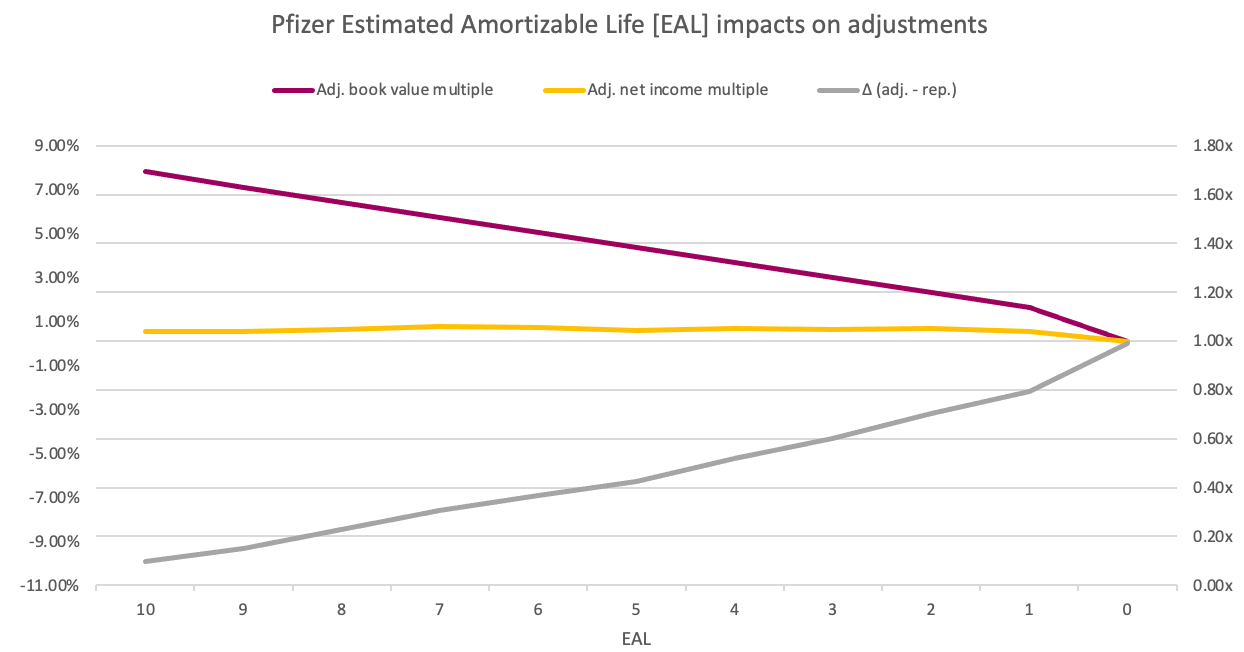

The impact is massive, with [1] “Adjusted book value” 69.32% higher (1.69x) than “Reported book value”, [2] “Adjusted net income” 3.90% higher (1.04x) than “Reported net income”, and [3] a negative difference of 9.91% between adjusted and reported return on equity.

This series of adjusted metrics picture a more realistic view of the real, underlying business conditions of Pfizer. That is, a significant understatement of book value, a modest understatement of net income, and a significant overstatement of return on equity.

Changing the EAL from 10 down to 1 reduces the impact on every one of the metrics analysed, converging towards the reported numbers for EAL = 0:

X axis = EAL; Left Y axis = ∆ (adj. - rep.); Right Y axis = Book value “Multiple” and Net income “Multiple”;

Industry findings

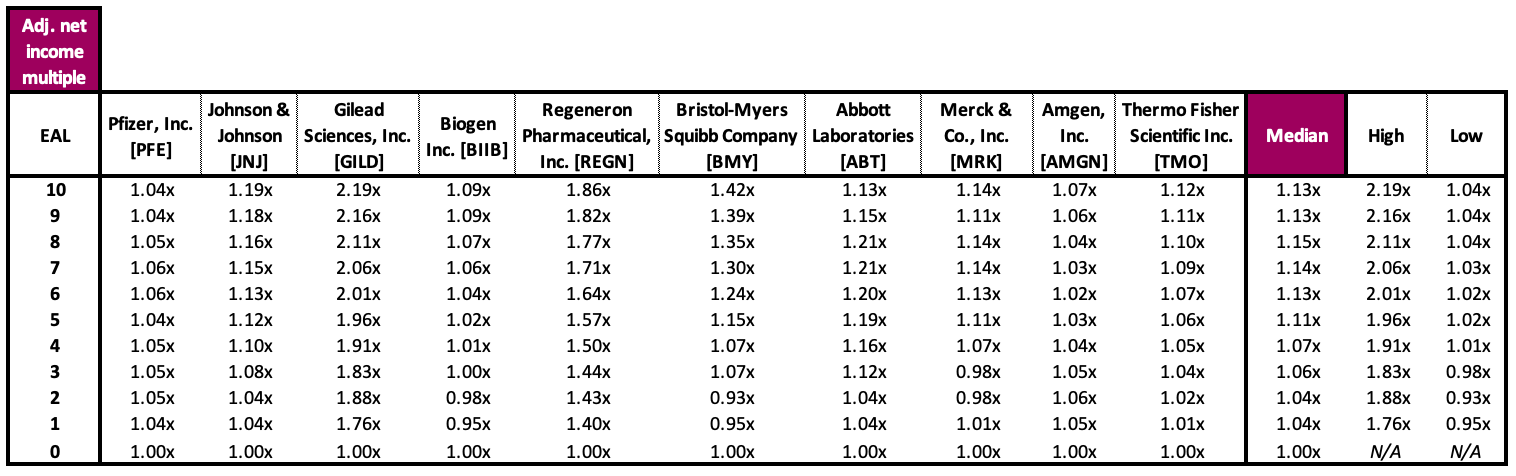

I’ve chosen a sample of companies in the industry and applied the same procedures to understand the impact of the inaccurate R&D treatment:

Pfizer, Inc. [PFE]

Johnson & Johnson [JNJ]

Gilead Sciences, Inc. [GILD]

Biogen Inc. [BIIB]

Regeneron Pharmaceutical, Inc. [REGN]

Bristol-Myers Squibb Company [BMY]

Abbott Laboratories [ABT]

Merck & Co., Inc. [MRK]

Amgen, Inc. [AMGN]

Thermo Fisher Scientific Inc. [TMO]

In the last three columns, I also calculated the median, high, and low number for each value of EAL:

Click here to download the model

As was predictable, the “Adj. book value multiple” is bigger for longer EAL, as R&D expenses depreciate at a lower rate. But the magnitude of changes is totally dependent on the relationship between reported book value and research & development spending, as shown by the differences in high and low values.

The results for the“Adj. net income multiple”:

The drivers behind the “Adj. net income multiple” are the current period R&D spending compared to previous periods spending. The adjustments can even go in negative territory in some cases, signaling an overstatement in reported net income.

Last but not least, “∆ (adj. - rep.)”:

Most of the values fall below zero, indicating an overstatement of return on equity in our sample. This overstatement is generally caused by the fact that book value is more understated compared to net income (also the reason why it goes further into the negative as you increase the EAL).

Conclusions

Under US GAAP, research and development is treated as an operating expense, when, in fact, according to the same GAAP definition, should be treated as a capital expense.

By capitalizing R&D, creating a research asset on the balance sheet that will be amortised over its Estimated Amortizable Life (EAL), and adjusting all of the three financial statements accordingly, we arrive at more precise representation of real, underlying business conditions.

This process of capitalizing R&D does in fact provide information that it is not entirely reflected in stock prices, as shown by Baruch Lev, Doron Nissim, Jacob Thomas “On the informational usefulness of R&D capitalization and amortization”.

This subtle difference has a profound effect on the reported financial statements of companies engaging in significant R&D spending:

median value in sample, assuming EAL = 10

Adjusted book value is 87% (1.87x) bigger than reported book value

Adjusted net income is 13% (1.13x) bigger than reported net income

The difference between adjusted and reported ROE is -5.68%

While the impact of capitalizing R&D varies across companies (and industries), we’ve found a general understatement of equity book value and net income and overstatement of return on equity in our sample.

It can even be argued that this process of capitalizing certain expenses and creating a corresponding intangible should be applied to [1] brand advertising expenses (Coca Cola marketing) that increase brand value over multiple periods, and [2] customer acquisition costs for businesses with recurring revenue streams (Netflix or any other SaaS) over multiple periods.

A good paper to further continue your reading on the subject: “Research and Development Expenses: Implications for Profitability Measurement and Valuation”, Aswath Damodaran

Thanks for reading.

Caveat emptor. Do not trust a 17 yrs. old on the internet. Do your own due diligence.